Emerging startups are going to try and figure out how to better encourage millennial homeownership

My top guess for 2020 is that we will see a handful of startups launch with the sole purpose of helping encourage millennial homeownership – either through savings paths, rent-to-own as a platform, shared equity, or alternative homeownership (shared vacation rentals and the like). Millennials are already the largest segment of consumers taking out new home loans (45% of all new home loans and 42% of loan values!), although only 32% of millennials actually own a home.

Banks will enable credit cards issuing via APIs

Deposit products have been the trendy product for the last several years, fueled by businesses built on interchange and neo-banks like Chime and Aspiration exploding in popularity. There are a dozen-plus APIs that exist for launching a deposit product – from Galileo to GreenDot to Evolve Bank – but there are hardly any that exist for credit cards. This will change in 2020.

There will be a surge of co-branded and private labeled credit cards launched by challenger banks and hot D2C brands

On that note, I’m bullish that we will see a surge of new co-branded and private label credit card launches in 2020. This will be encouraged by two trends:

Startups like Varo, Acorns, Chime, Aspiration, and others will look to diversify revenue through additional product launches and leverage their consumer-first approach to build better experiences

Trendy D2C brands will focus on brand affinity, repeat shopping, and lifestyle by building new experiences on top of credit cards. For example – a mid-tier Away Card for travel or an Infatuation Card for dining and exclusive access to restaurants

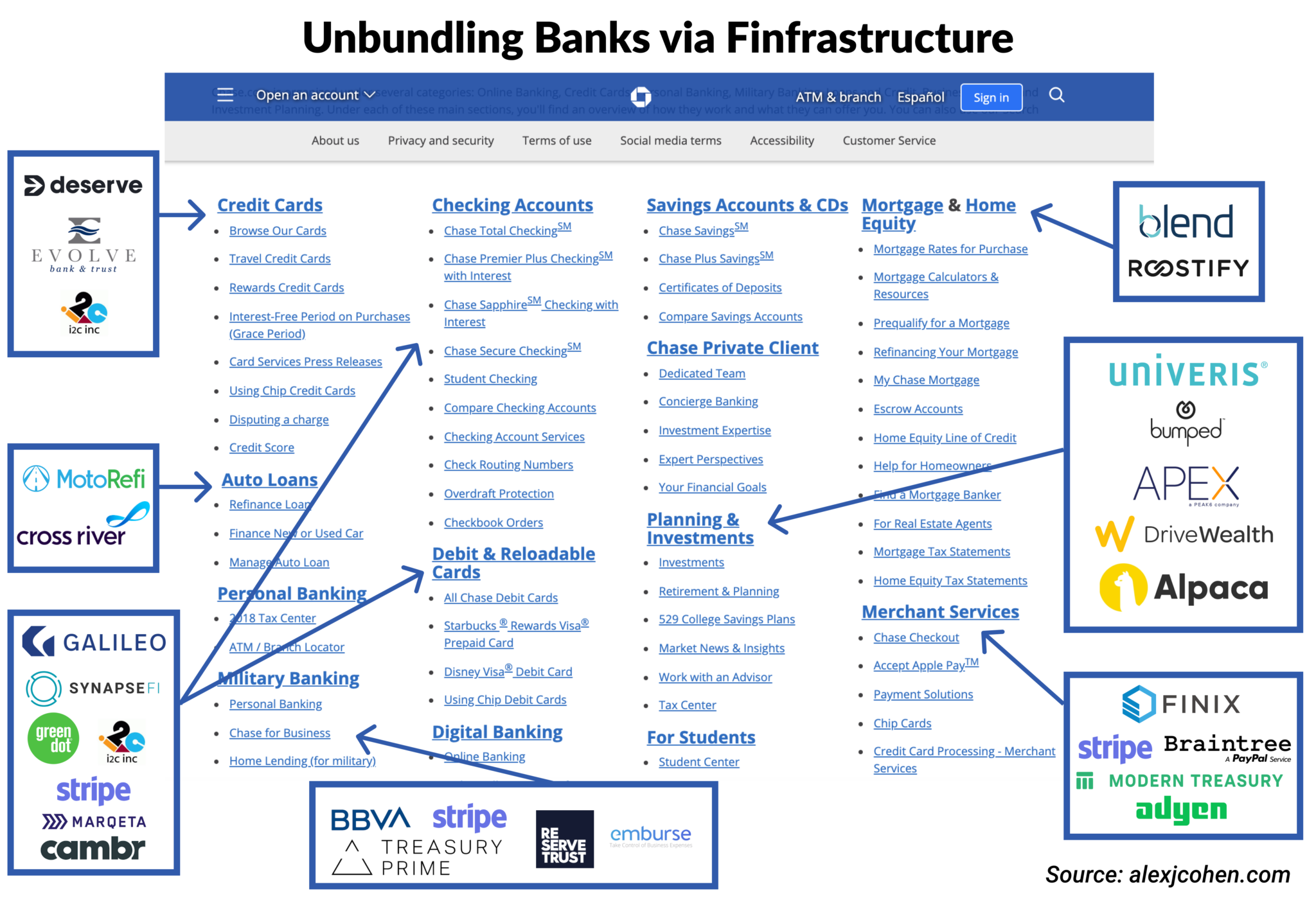

Fintech infrastructure will exist for every core banking product

2019 was a busy year for fintech infrastructure startups – Railsbank raised a $10m Series A, Galileo raised $77m, SynapseFi raised a $33m Series B, Cross River Bank is underwriting $1bn in loans per month, Modern Treasury raised a $10m Series A, Qwil raises $24.4m in equity and $200m in debt, among countless others.

I predict that we will see finfrastructure (you heard it here first) take off in 2020 and this will be the true impetus for “unbundling the banks”. Add this shit to your pitch decks:

More Consolidation

We saw a lot of M&A in 2019 and I expect this trend to continue. Even this week, Paypal announced that they were looking for more companies to acquire, fresh off of the $4bn acquisition of Honey and acquisition of GoPay.

Some notable acquisitions of 2019:

PayPal acquires Honey for $4bn

AON acquires CoverWallet

Q2 acquires PrecisionLender for $510m

Fox acquires Credible for $400m

H&R Block acquires Wave for $405m

FIS acquires WorldPay, Fiserv acquires First Data

Plaid acquires Quovo for $200m

Digital banks will find new distribution channels through offline & retail experiences

With rising customer acquisition costs for consumer financial services due to increased competition from both incumbent banks and more challenger banks, I expect to see digital banks fight for new eyeballs using more traditional methods – specifically offline (ATMs) and retail (the Moneygram and Western Union playbooks).

Given that most of these new digital banks target underbanked & underserved customers, distribution through retail to acquire the walk-in remittance market could be a great growth strategy. I hope we see interesting partnerships form here – Current & Safeway or Chime and Exxon as potential examples.

Also, don’t sleep on challenger bank ATMs to establish a physical presence + provide some unique brand affinity. Rural communities are already turning to grocery stores and high-fee ATMs as branches disappear.

Verticalized banking will continue to accelerate

Finally, I believe that we are only in the early stages of “banking for X”. I’m expecting a surge of verticalized banking that solves for a particular demographic. This tweet does a good job of breaking down markets that =1% of the population.

If I ever start a company, I think targeting a population that makes up ~1% of the US population is a nice target.

~2.6M Reg Nurses ~2.6M Farmers ~2.2M Active duty military & reserves ~3.2M Public school teachers ~3.5M Prof truck drivers ~3.7M High school graduates annually

Some of the above examples already have banking products that exist for their particular segments (military & education) but it highlights just how many people a product that serves just 1% of the population can be.

Check back Jan 1, 2021 to see how many of these I got wrong!

dreaming

dreaming